Most organizations think about transaction risk as a payment problem. In reality, risk exists throughout the entire transaction lifecycle.

As global trade shifts and businesses diversify suppliers, new counterparties are entering payment networks every day. Each new supplier relationship introduces new uncertainty, new operational complexity, and new transaction risk.

For banks, marketplaces, and B2B platforms, understanding where transactions fail and who absorbs the fallout is becoming increasingly important.

The Three Points Where B2B Transactions Break

The LiquidTrust Transaction Risk Map identifies three critical points where risk concentrates during the payment lifecycle.

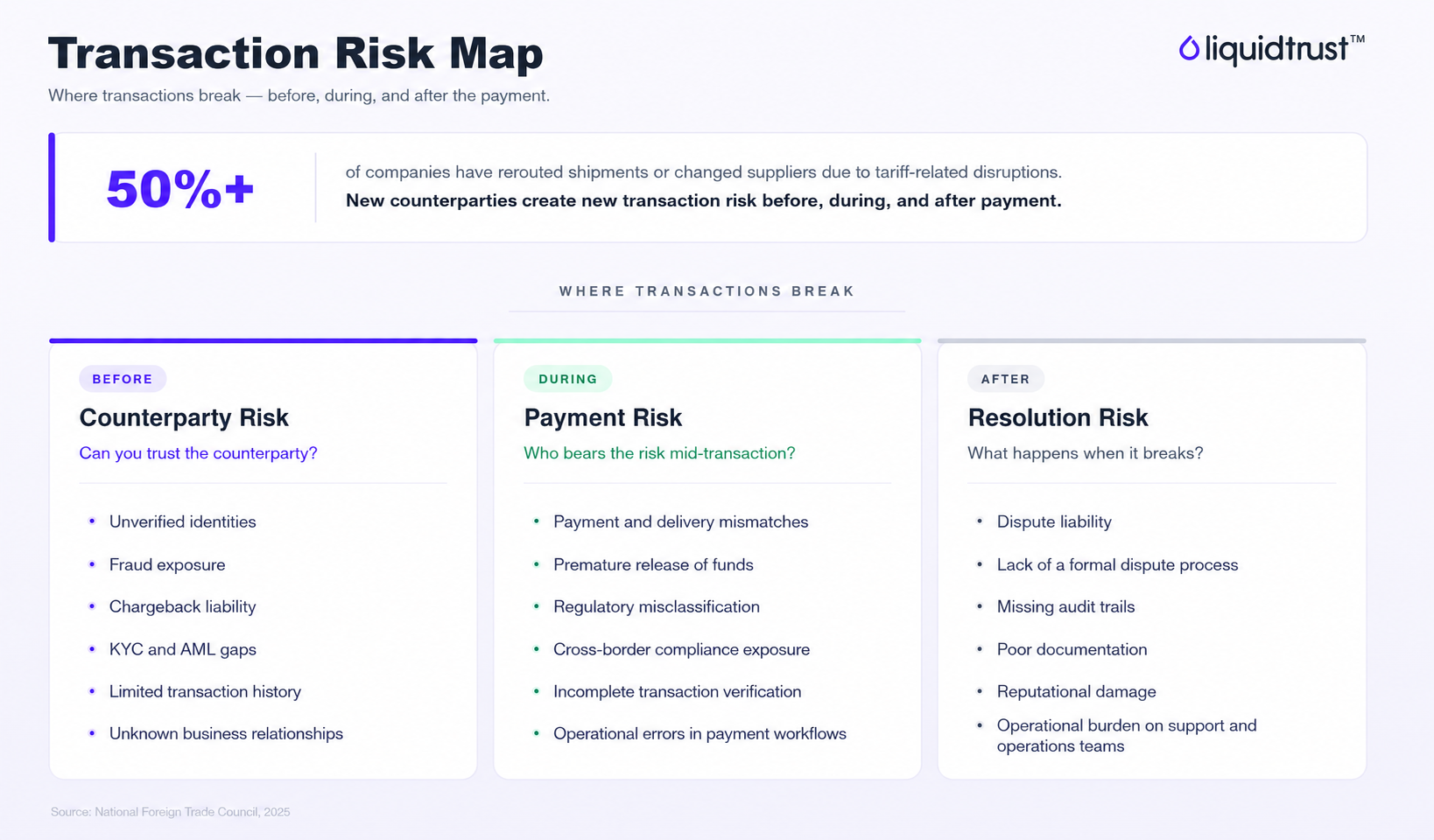

1. Counterparty Risk

Before money moves, the first question is simple: Can you trust the counterparty?

- Unverified identities

- Fraud exposure

- Chargeback liability

- KYC and AML gaps

- Limited transaction history

- Unknown business relationships

As businesses onboard new suppliers, distributors, and service providers and as marketplaces onboard new buyers and sellers they have never transacted with before, counterparty risk becomes the foundation for every transaction that follows.

2. Payment Risk

Once money begins moving, a new set of risks emerges.

- Payment and delivery mismatches

- Premature release of funds

- Regulatory misclassification

- Cross-border compliance exposure

- Incomplete transaction verification

- Operational errors in payment workflows

Many disputes originate during this stage because payments often move faster than trust.

Solutions such as Protected Pay and Micro Escrow help create structure around when funds move and under what conditions they are released.

3. Resolution Risk

The final stage occurs after money has moved. When a transaction breaks, organizations need a clear path to resolution.

- Dispute liability

- Lack of a formal dispute process

- Missing audit trails

- Poor documentation

- Reputational damage

- Operational burden on support and operations teams

Without a documented process, disputes become expensive, time-consuming, and difficult to resolve.

Why the Transaction Risk Map Matters

The Transaction Risk Map is built for the platforms and institutions that sit at the center of B2B commerce.

For banks, it provides a framework for helping clients understand where deals break and how payment infrastructure can reduce exposure.

For marketplaces and B2B platforms, it shows where the risk in a buyer-seller transaction lands on the platform itself. Moving money is the easy part. Fraud, disputes, compliance gaps, and operational load all collect around the deal and most of it lands on the operator in the middle.

The goal is not simply to move money. The goal is to build trust throughout the entire transaction lifecycle.

Because every transaction follows a lifecycle. And every lifecycle contains points where trust can break.